{kind=link}

Want better dividend checks without taking more risk?

Sector rotation for income investors means shifting money among the 11 major sectors as the economy changes to protect and grow dividend payouts.

Do it right and you keep cash flow when rates rise, grab higher yields in early recovery, and avoid painful dividend cuts in recessions.

This post shows the simple cycle signals and sector tilts that tend to boost realized income, and the trims and timing rules that stop you from locking in lower yields at the wrong moment.

Core Principles of Rotating Sectors to Enhance Portfolio Income

Sector rotation for income investors means moving capital between the 11 major stock sectors as the economic cycle shifts. We’re talking utilities, healthcare, consumer staples, REITs, financials, energy, materials, industrials, information technology, consumer discretionary, and communications. Unlike growth rotation that chases momentum, income rotation goes after sectors pumping out stable or rising dividend payouts. You’re protecting cash flow when things get rough and grabbing higher yields when cyclical opportunities open up.

Income investors rotate because dividend reliability swings with interest rates, inflation, and growth phases. When rates drop and recessions show up, defensive sectors like utilities and consumer staples keep paying even when sales slow. When the economy climbs out and credit loosens, financials and certain REITs can deliver yield expansion plus price recovery. Rotating with the cycle keeps your income stream alive and cuts the risk of permanent dividend cuts.

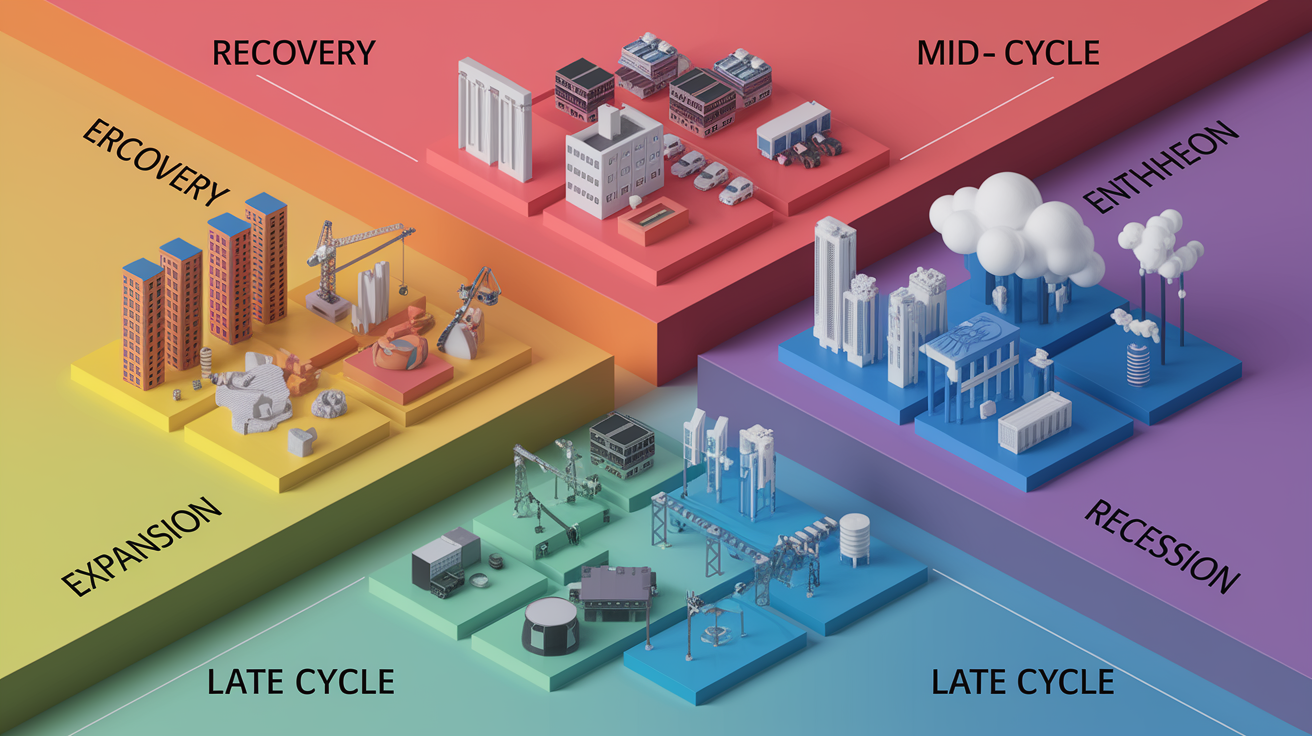

The economic cycle breaks into four stages, each running different lengths on average. Early recovery lasts about a year. Mid-cycle expansion averages 3.5 years. Late cycle runs roughly 1.5 years. Recessions compress below one year. Understanding these durations helps you judge when to tilt toward higher-yielding cyclicals and when to retreat into bond-like equities.

Six reasons income investors rotate sectors:

- Keep dividend purchasing power intact across rate cycles.

- Cut exposure to sectors facing margin pressure or earnings swings that threaten payouts.

- Grab early-cycle yield expansion in financials and REITs as rates stabilize and credit spreads tighten.

- Lock in late-cycle commodity-driven distributions from energy and materials before demand turns.

- Maintain total-return stability by mixing defensive yields with selective cyclical income.

- Avoid stacking too much into any single sector whose regulatory, competitive, or macro risks could hurt future dividends.

Economic Cycles and Their Impact on Sector Income Potential

Economic stages create distinct income environments. In early recovery (averaging one year), credit eases, loan growth restarts, and real estate values stabilize. Financials and REITs lead because rising loan volumes improve net interest margins for banks and falling cap rates lift property values. Materials follow as construction and industrial activity rebound. Jump in during this stage and you’ll capture dividend restarts and yield normalization after recession cuts.

Mid-cycle expansion, averaging 3.5 years, brings steady revenue and predictable cash flow. Healthcare, technology, communications services, and consumer discretionary benefit as corporate spending and consumer confidence rise. Dividend growth speeds up, but absolute yields often shrink as share prices climb faster than payout increases. Income investors hold these for dividend-growth continuity rather than high current yield.

| Stage | Duration | Leading Income Sectors | Typical Income Traits |

|---|---|---|---|

| Early / Recovery | ≈ 1 year | Financials, Materials, REITs, Consumer Discretionary | Dividend restarts, yield normalization, payout recovery from cuts |

| Mid / Expansion | ≈ 3.5 years | Healthcare, Information Technology, Communications, Consumer Discretionary | Stable dividends, dividend-growth acceleration, yield compression as prices rise |

| Late / Peak | ≈ 1.5 years | Energy, Industrials, Materials | High current yields from commodity cash flow, payout spikes, elevated volatility |

| Recession / Contraction | < 1 year | Utilities, Consumer Staples, Healthcare | Defensive yield stability, recession-resistant payout coverage, lower beta |

Late-cycle conditions, lasting about 1.5 years on average, see inflation pressure and tightening monetary policy. Energy, industrials, and materials thrive as commodity prices peak and producer margins widen. These sectors often offer high current yields, but volatility spikes and payout sustainability depends on how long commodity prices stay elevated. Recessions compress below one year and favor bond-like equities: utilities, consumer staples, and healthcare. Their essential products and regulated returns insulate dividends even as earnings stagnate.

Income-Rich Sectors and Their Role in Rotation Strategies

Utilities anchor income rotation. Regulated rate structures and essential-service demand create predictable cash flows that survive recessions. Stability makes them natural overweights when growth slows and rates fall. The Utilities Select Sector SPDR ETF (XLU) carries a 0.10 percent expense ratio and gives you broad exposure to electric, gas, and water providers. Because utility earnings correlate with interest-rate policy rather than economic activity, income investors pile into utilities when the Fed signals rate cuts or when inflation cools.

Consumer staples deliver similar defensive traits. Food, beverage, household, and personal-care companies maintain pricing power and volume even during downturns. The iShares US Consumer Staples ETF (IYK) has a 0.40 percent expense ratio and holds large-cap names with multi-decade dividend histories. Staples yield less than utilities but grow dividends more consistently, making them suitable when you want both current cash flow and long-term purchasing-power protection.

Healthcare combines recession resistance with demographic tailwinds. Pharmaceuticals, medical devices, and managed-care firms generate stable earnings because healthcare spending isn’t discretionary. The Invesco S&P 500 Equal Weight Health Care ETF (RSPH) charges 0.40 percent and provides diversified exposure without the mega-cap concentration of market-cap-weighted peers. Income investors favor healthcare during late-cycle uncertainty because dividends stay secure even if drug-pricing debates or regulatory shifts weigh on valuations.

REITs offer the highest yields among equity sectors but carry interest-rate sensitivity. Property types (residential, retail, industrial, office, data centers) react differently to lease structures and cap-rate moves. Falling rates compress cap rates and lift property values, boosting both dividends and share prices. Rising rates pressure long-duration REITs, especially those with floating-rate debt or short lease terms. Income investors screen REITs by lease duration, debt maturity profile, and occupancy trends, rotating into REITs early in recovery cycles and trimming when rate-hike cycles begin.

Five characteristics of stable sector income:

- Regulated or monopolistic revenue models that limit competitive pricing pressure.

- Non-cyclical demand tied to population growth, essential consumption, or infrastructure needs.

- Long-term contracts or subscription revenue that smooths quarterly earnings volatility.

- Low capital-intensity businesses that convert earnings into free cash flow without constant reinvestment.

- Management teams with established dividend policies and multi-year payout track records.

Interest-Rate and Inflation Effects on Income Sector Rotation

Interest-rate regimes dictate which sectors can sustain or grow income distributions. When rates rise, financials benefit because banks earn wider net interest margins on loans. Regional and large-cap banks increase dividends as loan portfolios reprice upward faster than deposit costs. Energy and materials also perform well in rising-rate environments because rate hikes typically coincide with strong demand and commodity-price inflation. Mortgage rates nearly doubled during the recent cycle, compressing housing activity and weighing on mortgage REITs and home-construction stocks, but benefiting energy producers whose products underpin industrial activity.

Falling rates create the opposite. Utilities, long-duration REITs, and bond-proxy equities rally because their fixed or slowly growing cash flows become more valuable when discounted at lower rates. Consumer staples and healthcare also benefit indirectly, as lower borrowing costs support consumer spending and corporate capital investment. Income investors rotate toward these sectors when the Fed signals rate cuts or when inflation readings fall below the 2 percent target.

| Rate Environment | Beneficiary Sectors | Hurt Sectors | Income Implications |

|---|---|---|---|

| Rising Rates | Financials, Energy, Materials | Utilities, Long-Duration REITs, Consumer Staples | Bank dividends expand; utility and REIT yields less attractive vs bonds; energy distributions spike |

| Falling Rates | Utilities, REITs, Consumer Staples, Healthcare | Financials (narrowing margins) | Bond-like equities rally; REIT cap rates compress, lifting distributions; bank dividend growth slows |

| Stable Low Rates | Balanced exposure; Healthcare, Communications, Tech | None (broad participation) | Dividend growth from earnings expansion; moderate volatility; high valuation multiples |

| High Inflation | Energy, Materials, select Industrials | Long-duration bonds, fixed-rate preferreds | Commodity-linked payouts surge; real yields on fixed income erode; nominal dividends lag inflation |

| Deflationary / Disinflation | Utilities, Staples, Investment-grade bonds | Energy, Cyclical Materials | Stable nominal dividends gain real purchasing power; commodity distributions collapse |

Inflation at a 40-year high during the recent cycle forced income investors to reconsider traditional defensive allocations. When inflation spikes, nominal dividends from utilities and staples lose real purchasing power unless companies can pass through cost increases. Energy and materials deliver inflation-hedged income because commodity prices and distributions rise with input costs. Income investors hedge inflation by rotating partial allocations into these sectors during early inflation signals, then trimming once inflation peaks and commodity prices roll over.

Timing Indicators Used by Income Investors to Rotate Sectors

Income investors rely on macro data and technical signals to time sector rotations. The primary macro indicator is the direction of Treasury yields. Sustained rising yields signal tightening financial conditions, prompting rotations from utilities and REITs into financials and energy. Falling yields indicate easing and favor defensive, high-dividend sectors. The 10-year minus 2-year Treasury spread (the yield curve) provides advance recession warnings. When the curve inverts (short rates exceed long rates), income investors start building positions in utilities, consumer staples, and healthcare ahead of the downturn.

Inflation readings versus the Fed’s 2 percent target drive rotation urgency. Core CPI prints above target accelerate Fed rate hikes, pressuring long-duration income sectors. Readings at or below target open the door for rate cuts, benefiting REITs and utilities. GDP growth trends confirm cycle stage. Accelerating growth supports cyclical income plays, while decelerating growth favors defensives. Employment data, manufacturing surveys (like ISM indexes), and consumer-spending reports offer real-time cycle verification. Mortgage-rate shifts directly affect housing-related income stocks, making mortgage-rate trends a key signal for REIT and home-construction sector rotations.

Technical indicators complement macro signals by identifying overbought or oversold conditions. The Relative Strength Index (RSI) measures momentum on a 0 to 100 scale. RSI readings at or above 70 indicate overbought conditions and potential rotation exits. RSI at or below 30 flags oversold levels and potential entry points. For example, the Consumer Staples Select Sector SPDR ETF (XLP) hit an RSI of about 74 in April 2022 and fell 12.3 percent in the month following April 20. XLP later touched RSI 23.7 on September 30 and rallied 15.7 percent within 60 days. On October 3, 2023, XLP bottomed at RSI 22 and rose roughly 2.4 percent since that date.

Seven timing indicators for income sector rotation:

- Trend in 10-year Treasury yield. Rising means rotate to financials/energy. Falling means rotate to utilities/REITs.

- 10-year minus 2-year yield spread. Inversion means add defensives. Steepening means add cyclicals.

- Core CPI vs Fed 2 percent target. Above means trim long-duration. At/below means add bond proxies.

- Quarterly GDP growth. Accelerating means increase cyclical income. Decelerating means increase defensive income.

- ISM Manufacturing PMI. Above 50 means industrial/materials. Below 50 means staples/utilities.

- Mortgage-rate moves. Doubling means reduce REITs. Stabilizing/falling means add REITs.

- 50-day / 200-day simple moving average crossovers. Golden cross means bullish sector entry. Death cross means exit or trim.

Moving-average crossovers confirm trend changes. A golden cross happens when the 50-day SMA crosses above the 200-day SMA, signaling upward momentum. A death cross (50-day falling below 200-day) warns of downtrend continuation. The Consumer Discretionary Select Sector SPDR ETF (XLY) formed a golden cross in May and broke out afterward, showing how technical signals validate macro rotation decisions.

Practical Portfolio Construction for Income-Focused Sector Rotation

Building an income-rotation portfolio starts with defining target allocation ranges for defensive, cyclical, and commodity-linked sectors. A baseline framework allocates 40 to 60 percent to defensive, high-income sectors: utilities, healthcare, consumer staples, and high-quality REITs. These anchor the portfolio and stabilize cash flow during downturns. Cyclical sectors (financials, consumer discretionary, and selective technology) get 20 to 40 percent, capturing yield expansion and dividend growth during recoveries. Commodity-oriented sectors (energy, materials, MLPs, and energy-infrastructure REITs) occupy 5 to 15 percent, providing inflation hedges and late-cycle income spikes.

Cash and short-term bonds fill the remaining 5 to 20 percent. Cash serves three purposes: downside protection during corrections, dry powder for opportunistic rotations, and yield from money-market funds when short rates rise. Income investors calibrate these ranges to personal risk tolerance, income needs, and time horizon. Younger investors seeking dividend growth might tilt toward the higher end of cyclical allocations. Retirees prioritizing stable monthly cash flow lean toward the defensive end.

Rebalancing triggers prevent drift and enforce discipline. Calendar-based rebalancing (quarterly or semi-annual reviews) keeps allocations within target bands. Trigger-based rebalancing activates when a sector weight deviates by 5 to 10 percentage points from its target or when key macro indicators flip. Examples: two consecutive Fed rate hikes or cuts, a CPI print that beats or misses estimates by more than 0.3 percentage points, an earnings-revision wave where analyst estimates shift by more than 5 percent across a sector, or mortgage rates moving by more than 50 basis points in a quarter.

| Portfolio Type | Defensive Allocation % | Cyclical Allocation % | Cash/Bonds % | Intended Use Case |

|---|---|---|---|---|

| Defensive Income Baseline | 55 | 25 | 20 | Recession hedge; maximum yield stability; capital preservation; retirees drawing income |

| Early Recovery Tilt | 40 | 45 | 15 | Soft landing expected; capture cyclical yield expansion; moderate risk tolerance; pre-retirees |

| Rising-Rate Environment | 30 | 50 (heavy financials/energy) | 20 | Fed tightening cycle; inflation above target; trim long-duration REITs; working professionals |

Risk management layers over allocation. Sector position caps (typically 25 to 35 percent per sector) prevent single-sector concentration. Individual security caps of 5 to 7 percent limit idiosyncratic dividend risk. Stop-loss rules or trailing-stop orders protect against sharp drawdowns, especially in volatile cyclical sectors. Stress-testing portfolio yield under recession assumptions (assuming 10 to 20 percent dividend cuts in cyclical holdings) validates whether total income meets minimum needs even in adverse scenarios.

ETF Tools and Screening Methods for Implementing Income Sector Rotation

Sector ETFs offer the fastest, most cost-effective rotation vehicles for income investors. Low expense ratios, instant diversification, and daily liquidity make ETFs ideal for tactical shifts. The Utilities Select Sector SPDR ETF (XLU) charges 0.10 percent and tracks large-cap utilities. The iShares US Consumer Staples ETF (IYK) and Invesco S&P 500 Equal Weight Health Care ETF (RSPH) each charge 0.40 percent, providing broad staples and healthcare exposure. For cyclical rotations, the iShares U.S. Financials ETF (IYF) at 0.40 percent, Fidelity MSCI Consumer Discretionary ETF (FDIS) at 0.08 percent, and Vanguard Consumer Discretionary ETF (VCR) at 0.10 percent deliver targeted sector access. Technology exposure through the Technology Select Sector SPDR ETF (XLK) at 0.10 percent rounds out growth-and-income blends.

Rotation-focused ETFs automate some tactical decision-making. Funds such as AESR, RORO, FCTR, SECT, and others employ momentum, relative-strength, or rules-based models to shift allocations across sectors. These rotation ETFs serve as benchmarks or as sleeves within a larger portfolio, letting income investors compare active decisions against systematic strategies. Mutual-fund alternatives (ATCIX, ATACX, CRTBX, QAISX, NAVFX) provide similar rotation exposure with active management and sometimes higher expense ratios, suitable for tax-deferred accounts where turnover doesn’t trigger immediate capital-gains taxes.

Screening tools help identify individual dividend stocks within target sectors. Online brokerage platforms and third-party screeners let investors filter the universe of 77,000-plus mutual funds and ETFs by sector, yield, payout ratio, dividend-growth rate, and expense ratio. For stock-level screening, filter by sector, minimum yield, payout ratio below 80 percent (to ensure coverage), and multi-year dividend history. Backtesting rotation models against historical data validates timing rules and allocation ranges. Many platforms offer strategy-tester modules that simulate periodic rebalancing, RSI-based entries, and moving-average signals across past cycles.

Six steps for screening and implementing income sector rotation:

- Define minimum yield threshold (e.g., 3 percent for defensive sectors, 2 percent for cyclicals) and maximum payout ratio (e.g., 75 percent to preserve dividend safety).

- Filter sector ETFs by expense ratio below 0.50 percent and average daily volume above $5 million for liquidity.

- Use stock screeners to identify individual holdings within target sectors, ranking by dividend-growth consistency and free-cash-flow coverage.

- Backtest proposed allocation ranges and rebalancing triggers over the prior two full economic cycles to measure income stability and drawdown risk.

- Monitor fund-flow data weekly to spot institutional rotation trends. Large inflows into defensive ETFs signal risk-off sentiment. Outflows indicate rotation toward cyclicals.

- Set calendar and trigger-based alerts for RSI extremes, moving-average crossovers, and macro-data releases (CPI, FOMC statements, GDP) to automate rotation-decision prompts.

Expense ratios matter for long-term income compounding. A 0.10 percent fee versus 0.40 percent saves 30 basis points annually, which compounds over decades. In taxable accounts, ETFs offer tax efficiency through in-kind redemption that defers capital gains. In tax-deferred IRAs or 401(k) accounts, individual dividend-growth stocks may outperform ETFs by avoiding the expense drag, but require more active monitoring and research.

Real-World Examples of Income-Driven Sector Rotation Scenarios

Picture an income investor entering 2023 with a portfolio weighted 50 percent utilities and consumer staples, 30 percent healthcare, and 20 percent cash. Data through September 30 showed economically sensitive sectors (communications services, information technology, and consumer discretionary) outperforming as tech rallied on artificial-intelligence enthusiasm. Inflation readings began falling below prior-year peaks, and the Fed signaled a pause in rate hikes. Recognizing the shift from late-cycle tightening toward potential soft landing, the investor rotated 15 percentage points from utilities into financials and consumer discretionary, capturing dividend expansion as banks resumed buybacks and retailers posted better-than-expected guidance. By maintaining a 35 percent defensive base, the investor preserved core income while participating in the recovery rally.

A second scenario unfolded in early 2022 when inflation spiked to a 40-year high and the Fed began the fastest rate-hike cycle in decades. An income investor holding 40 percent REITs and utilities saw those positions decline as mortgage rates nearly doubled and long-duration yields surged. Rotation signals (rising 10-year Treasury yields, CPI prints above 8 percent, and RSI readings above 70 in consumer staples) triggered a defensive reallocation. The investor trimmed REITs by 10 percentage points and added energy and financials, which benefited from commodity-price strength and expanding net interest margins. The energy allocation delivered high current yields and capital appreciation through mid-2022, offsetting losses in rate-sensitive sectors.

Five rotation flows in response to economic transitions:

- Late-cycle to soft landing: shift 10 to 15 percent from utilities/staples into financials, consumer discretionary, and select technology to capture yield expansion and dividend-growth acceleration.

- Late-cycle to recession: increase utilities, consumer staples, and healthcare to 55 to 60 percent; trim cyclicals to 20 percent; raise cash to 15 to 20 percent as downside buffer.

- Recession to early recovery: rotate 15 to 20 percent from staples/utilities into financials, REITs, and materials as credit spreads tighten and loan growth resumes; maintain 10 percent cash for further deployment.

- Mid-cycle inflation surge: add 10 to 15 percent energy and materials to hedge real-yield erosion; reduce long-duration REITs; hold healthcare for pricing-power stability.

- Mid-cycle disinflation: trim commodity sectors by 10 percent; reallocate to utilities and high-quality REITs as falling rates lift bond-proxy valuations; lock in higher yields in short-duration bonds.

These scenarios show the interplay of macro signals, technical indicators, and sector fundamentals. Successful rotations begin with clear entry and exit rules, disciplined rebalancing, and continuous monitoring of inflation, interest rates, and earnings trends.

Managing Key Risks When Rotating Sectors for Income Stability

Sector rotation carries execution, timing, and concentration risks that income investors must control. Economic cycles vary in length and character. Recent years saw pandemic stimulus create unprecedented household cash balances, split goods-versus-services demand, and a rolling recession that moved from manufacturing to technology to housing. Historical stage durations provide averages, not guarantees, and the source of a recession (credit crisis, oil shock, policy error) determines which sectors suffer most. Investors who rigidly follow cycle playbooks without adapting to current conditions can rotate too early or too late.

Tax consequences amplify rotation costs in taxable accounts. Profitable sector sales trigger short-term or long-term capital-gains taxes, reducing net returns. Frequent rotations compound tax drag, especially in rising markets where gains accumulate quickly. Income investors mitigate this by implementing rotations in tax-deferred IRAs or 401(k) accounts, using tax-loss harvesting to offset gains, and favoring ETFs over individual stocks in taxable accounts for in-kind redemption benefits. Setting higher rotation thresholds (like 10 percent sector drift instead of 5 percent) reduces turnover and preserves more after-tax income.

Diversification within sectors prevents single-stock dividend disasters. Sectors aren’t monolithic. Airlines and railroads both sit in industrials, but falling oil prices help airlines and hurt freight railroads. Mortgage REITs and data-center REITs respond differently to rate changes. Income investors screen individual holdings by payout ratio, debt levels, free-cash-flow coverage, and management track record, avoiding yield traps where high current dividends mask unsustainable payouts. Limiting individual positions to 5 to 7 percent and sector caps to 25 to 35 percent ensures that any single dividend cut or sector shock doesn’t derail total portfolio income.

Five essential risk controls for income-focused rotation:

- Apply strict sector and security position limits to prevent concentration. No more than 30 percent in any one sector, 7 percent in any single stock.

- Stress-test portfolio yield by assuming 15 percent dividend cuts in cyclical sectors and 5 percent cuts in defensives under recession scenarios. Verify remaining income meets minimum needs.

- Use a barbell allocation. Pair recession-resistant sectors (40 to 50 percent) with selective cyclical exposure (25 to 35 percent) to balance stability and opportunity.

- Maintain 10 to 20 percent in cash or short-term bonds as both downside buffer and rotation capital, redeploying when RSI extremes or macro signals trigger entries.

- Implement tax-aware rotation strategies. Execute high-turnover moves in tax-deferred accounts, harvest losses in taxable accounts, and favor low-turnover core holdings for long-term capital-gains treatment.

Drawdown discipline protects capital and income. Trailing stop-loss orders (set 10 to 15 percent below entry prices in cyclical sectors) automatically exit positions during sharp corrections. Income investors review stops quarterly and adjust for volatility. Defensive sectors tolerate tighter stops (8 to 10 percent) due to lower expected volatility, while energy and materials warrant wider stops (12 to 18 percent) given commodity-price swings. Regular stress tests using recession assumptions, rising-rate scenarios, and dividend-cut histories validate whether the portfolio can sustain target income levels across cycle turns.

Final Words

We walked through why shifting among utilities, healthcare, REITs, financials and energy smooths dividend payouts as the economy turns.

You got the cycle map, timing signals to lean on, ETF tools to execute, and portfolio frameworks to manage drawdowns and taxes.

Use what fits your goals: set allocation ranges, rebalance on clear triggers, and stress-test yields before moving.

Practical rotation, not guesswork. sector rotation for income investors can raise reliability and reduce surprise — a clear path to steadier dividend income.

FAQ

Q: What is the 3-5-7 rule in investing?

A: The 3-5-7 rule in investing is a simple time-horizon guideline: use about 3 years for short-term, 5 years for medium-term, and 7+ years for long-term when matching assets to goals.

Q: What is Warren Buffett’s 90/10 rule?

A: Warren Buffett’s 90/10 rule is a basic allocation: put 90% in a low-cost S&P 500 index fund and 10% in short-term government bonds or cash for a low-cost, long-term core portfolio.

Q: What is sector rotation in investing?

A: Sector rotation in investing is the practice of shifting weights among industry sectors as the economic cycle changes, moving into sectors likely to outperform and away from those likely to lag.

Q: What sector is going to boom in 2026?

A: There’s no obvious consensus on which sector will boom in 2026; likely candidates include AI/semiconductors (tech) if innovation stays strong, or energy/materials if commodity prices and late-cycle forces dominate.